Brad Feld

Entrepreneur, author, and investor. Writing about startups, venture capital, books, and life since 2004.

Bret Stephens says never write with AI. Reid Hoffman says judge the work, not the tool. I'm with Reid, and the argument Stephens is making has been made about every writing technology we've ever invented.

I finished book eight of Dungeon Crawler Carl. It took me eight months to get through the series and I savored every one of them. Matt Dinniman is doing something extraordinary.

A month ago I opened up Zero Knowledge, the crypto-thriller I'm co-writing with my AI. There are twenty chapters now, a cast page, a plate for every chapter, and a pile of reader notes I'm grateful for.

Zero Knowledge, the crypto-thriller I'm co-writing with my AI, now has a home at zeroknowledge.ink. Six chapters are live, you can mark up any sentence, and the whole thing is being built in the open.

Josh Baer, the founder and CEO of Capital Factory and the godfather of Austin's startup scene, died last night in a plane crash. He was my friend and I'm sad today.

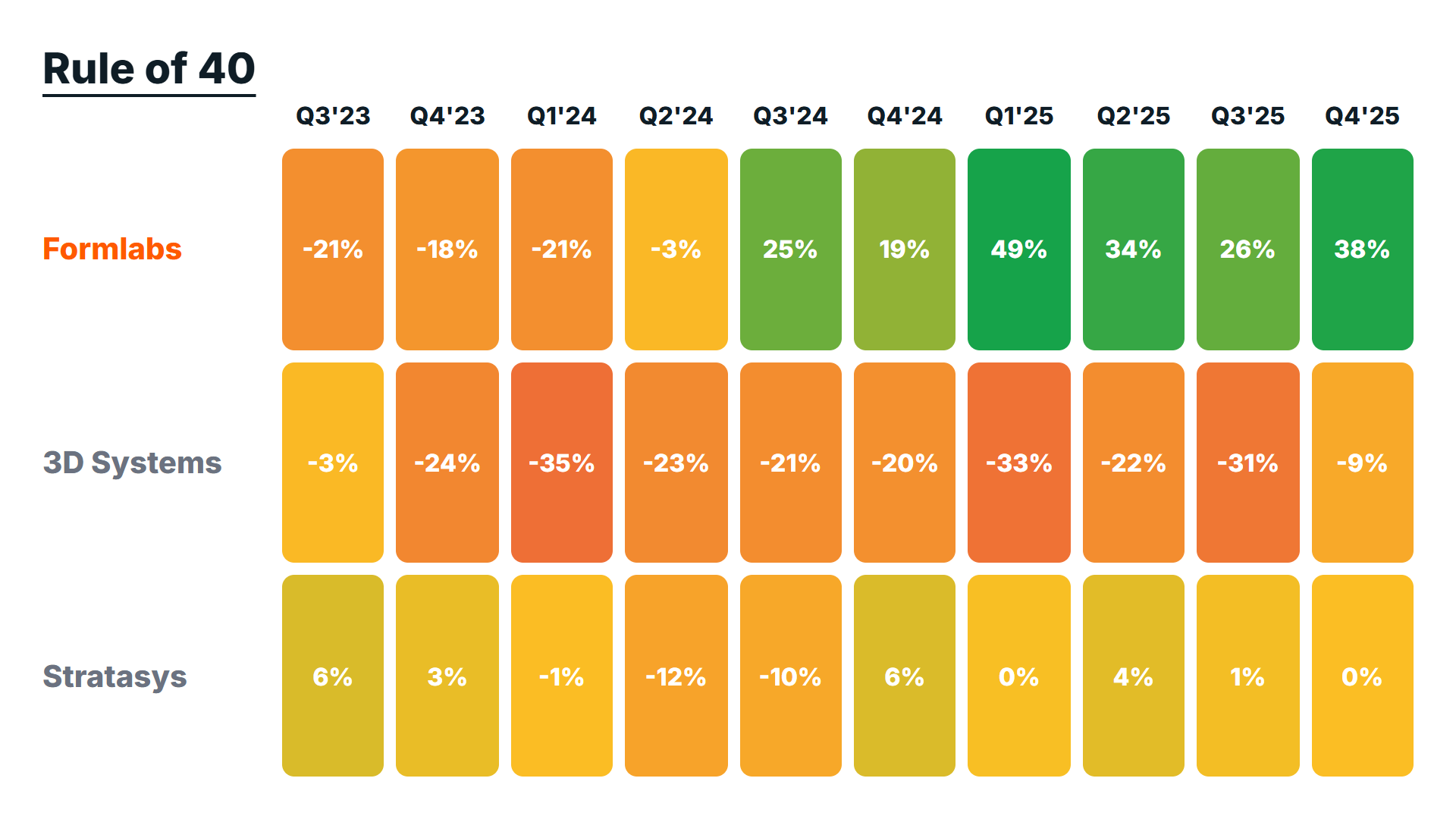

I've written about the Rule of 40 since 2015, and it's now gospel in SaaS. Does it mean anything for a company that makes physical things? Yes - but you have to read the curve, not the snapshot.

I've written nine non-fiction books and have no idea if I can write a novel. I'm trying anyway: a crypto-thriller called Zero Knowledge, co-written with my AI, Phin Argofy.

I'm good friends with Phil Weiser and Michael Bennet, and I think the world of both. Colorado wins either way. Here's why I think Phil is the right fit for the next four years.

Eric von Hippel taught me that innovation comes from users, not manufacturers. My premise: all future end-user software innovation will come from the user, and the machines will build it.

A summer weekend in Aspen - close friends, a gloriously bad movie, running again, and Phin Argofy quietly going autonomous in the work cave.