Tag: finance fridays

Our friends Dick and Jane have decided to disband their company. The last two months had been tough for Dick and Jane – each of them felt the other wasn’t living up to their commitments. Praveena was working hard on the product, but as she observed the tension mounting between Dick and Jane, she started answering calls and emails from the recruiters who had been hounding her since she left her previous job.

One night, a few weeks ago, Dick finally acknowledged to Jane that he was feeling incredible financial pressure. Dick and his wife Mary never really had agreed that Dick should take the plunge and start SayAhh. Dick was struggling to admit that he wasn’t fully committed to this path, even though he had been really excited about starting the company. While he was taking a salary, it was modest, didn’t cover his monthly expenses, and the combination of financial and daily work pressure were causing a lot of friction at home. Dick told Jane that Mary was being awesome and that she’d keep being supportive, but it wasn’t working for them as a couple.

Jane was surprised but calm. She felt it was important to bring Praveena into the loop since since they were all partners now. Over dinner, Dick, Jane, and Praveena discussed where they were at and how Dick was feeling. Praveena acknowledged that, while her relationship wasn’t causing any stress (she was involved with the founder of another company) she was having a lot of trouble working in the unstructured environment of a startup. She admitted that she was having serious conversations with a very large technology company in town about joining them as a PM for a product she was really excited about. Dinner went on a long time, had a lot of emotion in it, but ended without any specific resolution.

Jane didn’t sleep at all that night. She couldn’t believe that she’d missed these signals with each of her partners. She thought they were each as committed to SayAhh as she was. She went through a huge range of emotions dominated by anger, frustration, sadness, and depression before getting a clear grip on what she wanted to do just as the sun started coming up. A mentor of her’s once said “don’t ever make a final decision when you are tired” and she wanted to heed that, so she decided to tell Dick and Praveena what she was thinking when they got to the office, but leave it open for a final decision through the end of the weekend.

The conversation in the office was anti-climactic. Each of the partners had the same sleeplessness night and they all shared that as hard as it was to admit, they didn’t feel like they could go forward as a team for various reasons. It was not an angry conversation, but it was a sad one. But honest. They agreed to disband for the weekend (it was Thursday), have a long, quiet time thinking over what they wanted to do, and get back together first thing Monday morning.

On Monday, at 9am, Dick, Jane, and Praveena decided to shut SayAhh down. Dick had already talked to his previous boss who welcomed him back if he wanted to come back. Praveena had gotten a final offer from BigTechCo which she had a week to accept. And Jane had decided that she wanted to keep working on a startup, but wanted to hit reset, find different co-founders, and take more time making sure the idea was sound before they started spending any money.

They had $32,000 left of the original $70,000 in the bank after paying off all of their bills. The founders decided to split the remaining $32,000 between Jane and Praveena based on their capital investment, so Jane got 5/7ths and Praveena got 2/7ths. Jane took on the task of winding everything down, sending out notes to all of the people who had helped them, and Dick, Jane, and Praveena agreed to collectively hold their heads high, stay friends, and be glad that they called it quits before things spun out of control.

While Jane was building SayAhh’s revenue projections, Dick focused his attention on building the expense side of the projections. He procrastinated for a few weeks because he was deep in product development, but surfaced a few days ago when he realized they had an investor meeting coming up and really should have at least a basic financial model ready in case the investor asked about it.

Before building his projections, Dick needs to make three main decisions:

- Should he build a simple cash forecast or a set of projected financial statements?

- What are the right drivers for each expense category?

- How should he account for unforeseen expenses?

1. Cash Forecast vs. Projected Financials – What’s the difference?

A simple cash forecast is just that – it is a model that helps anticipate cash balances over time. It is simple in that it forecasts how much cash will be coming in the door (revenues + equity financing + debt financing) and then subtracts from that amount how much cash is expected to be going out the door. The expense forecast tends to be organized by what the money is being spent on such as office space, employee salaries, or computer hardware and software.

Building a set of projected financial statements is more complicated. For one, it requires keeping track of not only what the company is going to be buying, but also where the purchased goods/services are used. In the straightforward example of a widget manufacturer, expenditures on electricity (the “what”) can get spread across multiple line items on the Income Statement. Part of the spend may be assigned to Cost of Goods Sold, part to Marketing, and part to General & Administrative, all of which can be separate line items on the Income Statement (the “where”).

Creating a set of projected financial statements also requires understanding different types of expenses. Specifically, is an expense an operating expense (generally speaking, spend on a good or service that is consumed immediately) or a capital expense (spend on an asset that will be used up more gradually over time)? The former will impact the Income Statement, Balance Sheet, and Cash Flow Statement while the latter will only impact the Balance Sheet and Cash Flow Statement (although as the asset depreciates, the depreciation will show up on the Income Statement).

To keep track of all of this, companies assign every expense to a Cost Center (tells where the spending occurs, indicating the line item on the Income Statement that will be impacted), a Cost Code (which indicates what was purchased, e.g. Office Supplies, Salaries, Utilities, etc.) and a spend type (e.g. Capital vs. Operating).

Finally, building projected financials requires a strong understanding of the interactions between the three financial statements.

Due to the added complexity of building projected financial statements and because Dick and Jane are currently focused on cash, Dick chose to build a cash forecast. This is fine for now, but eventually SayAhh will need to become sophisticated enough to build projected financial statements.

2. Choosing the right drivers for each expense category

Just as it was important for Jane to choose the right drivers for her revenue projections, it is similarly important for Dick to choose the right drivers for his expense forecast. Since this was addressed on the revenue side, we won’t go into details on the expense side.

3. Accounting for unforeseen expenses

Dick is confident that his forecast will capture SayAhh’s major business expenses. But how should he forecast unanticipated expenses? Dick decided that unanticipated expenses will be equal to 10% of anticipated expenses in order to provide a cushion in SayAhh’s budget.

4. Putting it all together

With that, SayAhh now has their initial set of revenue & expense projections. Subtracting the expenses from the revenues provides a forecast of cash flow from operations. Dick and Jane are not currently anticipating any additional cash flow from financing (or investments), so these projections are a good indication of SayAhh’s anticipated cash burn, which will help Dick and Jane determine when/if they need to raise more money.

Since last checking in with the SayAhh team, they have spent a few months consumed with building an early version of the product and speaking to potential customers, all the while watching their cash balance steadily diminish. They realize the clock is ticking and have decided that it is time to create a robust set of financial projections in order to provide themselves with a better sense of when they will need to raise more money.

The co-founders decided to divide-and-conquer, with Dick tackling expense projections and Jane tackling revenue projections. Their plan was to combine the two in order to predict their cash burn over the next two years (with a focus on the next twelve months). Jane asked Josh, who provided SayAhh with solid advice on setting up their accounting systems, for help in creating the revenue side of their financial forecast. Josh told Jane to take a first shot and he would comment. Here’s a snapshot of what Jane produced:

Josh worded his feedback carefully:

“Jane, this is a good start. I am glad to see that you are forecasting revenues based on business drivers. In this case, the # of users and the average monthly revenue per user. That’s what you should be doing. However, do you really understand the key underlying drivers of your business? Based on the drivers you chose, I am not so sure you do.

Certainly the # of users matters. But take it a step further. What drives the # of users? Presumably you will have new users, return users, and lost users each month. Decomposing users into these three component parts is important because it will allow you to better understand what is going on with your business, which will in turn allow you develop actionable strategies for improving your business.

For example, assume the # users remains flat for four months in a row. If you only track monthly users, you might assume that you are not attracting any new users and you need to change your marketing approach. However, what if it turns out that your marketing approach is just fine and you are bringing in lots of new users every month, but at the same time you are losing an equal number of existing users? In that case, the problem is that users don’t like your product. You need to fix that problem, not adjust your marketing approach. Take another shot at this and come back to me with a model that you think drills down to the key drivers of your business.”

Jane did some research, had a nice glass of wine, and really thought through their business model. Then she came back to Josh with a revenue model built on a set of key business drivers:

Josh told Jane that her second effort was much better and Jane in turn felt that she now had a much better understanding of SayAhh’s business model. A skeptic might assert that it is a waste of time for a pre-customer startup to forecast revenues since they are guaranteed to be incorrect. When I look at a startup’s revenue projections, I don’t pay much attention to the actual numbers for just that reason. However, I do look at the structure of the model to see if they really understand their business and are actively tracking their key business drivers.

In the next post, we will see how Dick fares with the expense forecast.

Note that Jane’s second attempt is a step in the right direction, but by no means perfect. Tying the number of new users to advertising spend seems particularly questionable, for example. What other problems do you see? What has been your experience/advice in developing revenue projections?

Now that Dick and Jane have added a CTO to SayAhh’s founding team, they’ve turned their full attention to working on their product. Today, we’ll look at the impact of the expenses to date on the P&L, Balance Sheet, and Cash Flow Statement.

Since SayAhh is in the pre-launch development stage, the company doesn’t have any revenue yet. They also haven’t launched a product, so there is no corresponding “cost of goods sold” – the direct cost of delivering their product. This results in a gross margin of $0, where gross margin is revenue – cost of goods sold.

The default Quickbooks setup uses “Income” to refer to “Revenue”. Since the Income (“Revenue”) line is $0 and the the gross margin is $0, Dick and Jane haven’t really noticed this yet. For now, we’ll leave it as is but once Dick and Jane meet with a mentor who is a CFO we expect this will change.

As of Aug 31st, here is their P&L.

The largest expense a company usually has at this stage is salaries. However, Dick, Jane and Praveena have decided to initially forgo salaries which helps them conserve cash in the near term. A company at this stage could also face product development costs from consultants if they decided to outsource product development. However, Praveena has committed to personally get the first version of the product up and launched without outside consultants, so there is no expense here either.

The largest expense a company usually has at this stage is salaries. However, Dick, Jane and Praveena have decided to initially forgo salaries which helps them conserve cash in the near term. A company at this stage could also face product development costs from consultants if they decided to outsource product development. However, Praveena has committed to personally get the first version of the product up and launched without outside consultants, so there is no expense here either.

Dick is focusing his effort on getting some early customer validation and is using a Lean Startup approach. Dick’s friend Samir, who is hoping to land a job with Sayahh, agreed to put together several static landing pages and email collection forms. Once these were up Dick launched several AdWords campaigns to test customer interest.

Dick, Jane, and Praveena decided to get a small office so they could work out of the same space. Dick recently had a child and didn’t want to use his house as it was too distracting, and both Jane and Praveena felt like their apartments were too small to all cram into. They made the decision that being together every day was better than working separately, so they signed a 1-year lease at $1500/month (prorated from mid-August) and they invested $1930 in capital improvements to remodel the entryway and install a sign. After signing the lease, Samir suggested that they could have saved a lot of money by using a co-working space but once the decision was made and the lease signed, there was no turning back.

In addition to the capital improvements (which show up on the balance sheet below as “Leasehold Improvements”) our fearless founders bought some tables, chairs, and a few other random things at Office Depot. Both the renovations and furniture purchases are “capitalized” on their balance sheet rather than being expenses on the P&L. While the cash is gone, the “expense” is “depreciated” over several years (depending on the type of asset).

Following is the balance sheet and the changes from July to August.

Our founders had some other expenses, including business cards and a trip to an industry conference where they talked to a number of potential customers. While the conference was educational, Dick and Jane were frustrated with the dull gaze they got from uninterested prospects when they tried to explain what they were doing, but couldn’t actually show anything. On the flight home from the conference, Dick and Jane agreed they both needed to help Praveena get the first product out, whatever it took.

Following is the third key financial statement – the Statement of Cash Flows.

In total, SayAhh burned through over $8000 during the month. Annualizing this number, SayAhh could expect around $96,000 in negative cash flow for the year. However, Jane realized that $3430 associated with the new office space security deposit and rennovations is essentially a one-time expense. This resulted in an annualized burn rate more in the neighborhood of $55,200 ($4,600 * 12).

As Finance Fridays continues, we are introducing the concept of the Cap Table. We recognize that we are still at the very early basics stage, but as we are taking a case study approach to this we feel like we have to set up all of the pieces before we get into the messy guts. Hopefully you are staying with us and finding this useful – feedback welcome!

Jane and Dick, our fearless cofounders of SayAhh, have set up an accounting system and created their first set of financial statements. This week they set out to create their cap table and hire a CTO.

The founders each have common shares that will vest over four years. The vesting schedule protects each of the co-founders in case one gets hit by a bus or decides to drop the project after a short period of time. Also, there is an important tax election called an 83(b) election that they made which allows them to recognize and pay taxes for very small income of the value of the shares. Later, if they sell, the low tax basis and capital gains tax rates result in a lower tax liability than if they didn’t file the 83(b) election.

Equity is split 55% and 45%, but where is that officially recorded? It is not in the three primary financial statements (the Balance Sheet, Profit & Loss, and Cash Flow Statement.) Rather, it gets recorded in a document called the Capitalization Table (or “Cap Table”), which shows the ownership stake each person or entity has in the business.

Below you can see Jane and Dick own 55% and 45%, respectively. As first time entrepreneurs they did not create an employee options pool; we’ll fix that in a little while.

Jane and Dick want to bring in their friend Praveena as CTO, but they don’t know how to structure the compensation. They come up with two options:

- Hire Praveena as an employee and offer her stock options.

- Bring Praveena in as a founder and offer 10-20% of the company as stock.

The benefit of hiring Praveena is they think they could keep more equity and control of the company. But, Praveena hails from the land of big paychecks and is not ready to leave that without considerable equity. With the funds Jane and Dick have, a big salary is not possible. Praveena wants to invest $20,000 and get 20% equity.

After several discussions (and more beer), Jane and Dick agreed with Praveena to bring her on as a cofounder where she invests $20,000 and also gets 15% equity. Praveena is just like the other two founders, where her equity will vest over 4 years. Time to update the cap table.

When you read the cap table, think of it as a series of events that add new columns to the right. Now there are two events: the initial issuance of founders common shares, and then issuing new founders common shares along with creating an options pool. In this manner, you can see both the current equity distribution of the company, as well as historically what the equity holdings looked like.

If the full pool were to be given out, the dilution is fairly significant to the founders. They would own from 55% and 45% down to 36% and 29%, but until options are exercised they are not diluted. Jane and Dick contemplated a small option pool because they had read about the risk of an option pool shuffle, but ultimately decided to make it 20% based on feedback from their friend Josh, a Boston-based venture capitalist.

Our (now three) co-founders begin building out their product. The co-founders have savings to live off of and cash will be conserved by not having any salaries. Next week we will fast forward to when they have a beta product and they build a model to pitch to investors.

When we were last with our SayAhh cofounders, they had implemented an accounting system and Jane had contributed $50,000 for a 55/45% equity split. This week we introduce two of SayAhh’s key accounting documents: the Balance Sheet (BS) and Statement of Cash Flows (SCF) showing how this investment is accounted for.

The investments by the founders created two transactions. Since SayAhh is a C corporation that is incorporated in Delaware, they decided to have a very low non-zero par value for their shares, set at $0.00001, to prevent higher franchise stock taxes. Thus for the 10M shares issued to the them, Jane invests $55 and Dick invests $45. Jane also invests $50,000 as previously agreed. These deposits increase the checking account balance and also the equity accounts, and results in a solvent company and a decent starting bank balance.

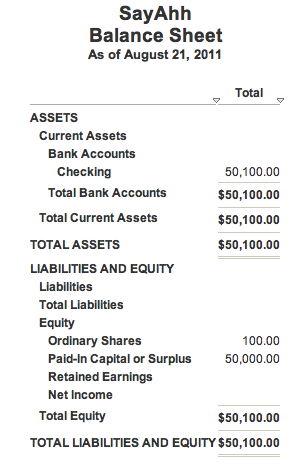

Below is the Balance Sheet as of 8/21/11. Fred Wilson’s MBA Mondays series shows how to think about the balance sheet – namely as a picture of the company at a point in time.

The Balance Sheet respects something called the Basic Accounting Equation. The Basic Accounting Equation states that Total Assets always must equal Total Liabilities plus Equity. In SayAhh’s case, you can see that the assets (cash in a checking account) equals liabilities (zero) plus equity. Assets = Liabilities + Equity.

If you use spreadsheets to keep track of your books, you could accidentally violate the Basic Accounting Equation, but not in accounting software program. This is one of the reasons that Dick and Jane chose to use QuickBooks, even at this very early stage, as it guarantees that their books will conform to double entry accounting.

Equity is comprised of two things. The Ordinary Shares equity account represent the par value paid by Jane and Dick for their 10M shares ($100). The Paid-In Capital account shows Jane paid in an additional $50,000. Combined these two amounts equal total equity, or $50,100.

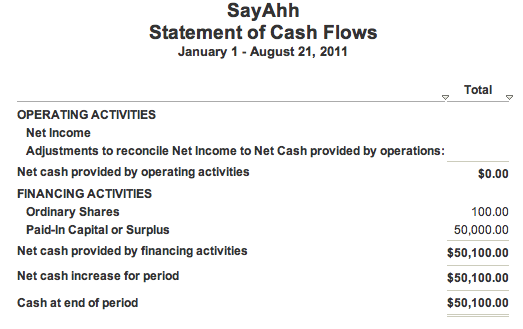

The other accounting document we are introducing today is the Statement of Cash Flows (SCF). The SCF breaks down how changes in balance sheet accounts and income affect cash. When presented in the SCF, these transactions are broken down into three categories: operating, financing and investing activities. Note the interconnected nature between these statements. The net $50,100 from financing activities all went into equity on the Balance Sheet.

Currently, SayAhh’s financials are very straightforward – even boring, but we’ve got to start somewhere. Next week we will introduce the Cap Table, and show how it changes when adding a co-founder.

When we were last with Dick and Jane on Finance Fridays, our fearless entrepreneurs were figuring out how to split up their founders equity and account for an investment from Jane. While they’ve been hard at work on their product, they’ve also incorporated the company, now named SayAhh (thanks Mac!) as a C-Corp in Delaware. They’ve done a bunch of other mundane things, such as establishing a business checking account and depositing Jane’s $50k in seed capital, but like all good early stage entrepreneurs, they’ve spent most of their time obsessing about their product, talking to a few potential early customers about what they needed, and coding away on their MVP.

Dick and Jane had limited formal business accounting experience, but they both knew how to balance a checkbook. They reached out to their friend John, a CFO at a late-stage VC-backed company in Boston that was about to file an S-1 to go public. John took an hour out of his day to do a conference call with Dick and gave them advice on how to set up their accounting system. His advice included the following,

- Set up a double-entry accounting system and use it to track all financial transactions.

- Build a financial model that forecasts the P&L. Revenues and costs should both be based off of a robust set of assumptions. This should tie to your GL for “Actuals” (i.e. historical data).

- Be sure to use accrual accounting, not cash accounting.

- Tie the P&L forecast to the Balance Sheet and Cash Flow Statement and generate snapshots of what the Financial Statements will look like each year for the next 5 years. Create monthly snapshots on a rolling 12 month basis.

- Anytime the financial model indicates that SayAhh will run out of cash, determine how you will raise capital to ensure liquidity and be sure to properly account for the debt or equity transaction on the balance sheet and Cap Table.

- Tie each round of funding to a set of key milestones in the development of your product/business.

John also mentioned a bunch of other stuff that Dick didn’t write down because they weren’t really sure what it meant, but it included phrases like 409a and VSOE. Feeling overwhelmed, Dick emailed his friend Josh, the CEO of an early-stage startup in Boulder, to see how they figured out all of this stuff. He summarized Dick’s advice and Josh replied: “That’s great advice and you should do all of that stuff – eventually. But, for now, focus on the following:”

- Make sure you both have business credit/debit cards and that you use them (or checks) for all transactions.

- Setup a simple accounting system like QuickBooks and sync it with your bank account. At the end of each week, make sure you’ve properly labeled each transaction using the QuickBooks Chart of Accounts. This takes a little getting used to, but you’ll pick it up. Ask me if you have questions.

- QuickBooks allows you to forecast expenses. Think through all of the expenses that you anticipate over the next 12 months and enter them. Update this every time you become aware of new transactions and maintain this on a rolling basis. QuickBooks will show you if/when you will run out of cash within the next 12 months.

- Build a plan as to how you will inject more cash into the business any time QuickBooks shows you running out of cash, and be sure to start raising any needed cash well in advance.

Dick and Jane followed Josh’s advice. It required a small investment of time and money to get QuickBooks up and running, but it was a manageable distraction from building SayAhh’s core product.

To be successful, you need to know about a wide range of issues affecting your business. However, you do not have to become an expert on each and the degree to which you need to understand various issues evolves along with your business. It is easy to get caught up in all the administrivia of of forming a company, building a business plan, and developing financial forecasts that you fail to spend time building your product.

How do you know what matters most when? This is where developing a network of trusted and qualified mentors comes in handy. While John was trying to be helpful, his advice missed the mark because he didn’t have a lot of experience at the early stages. In contrast, Josh was an experienced entrepreneur who had started several companies and likely learned his lessons through experience. As you build your business, surround yourself with as many Josh’s as you can. And, as you grow, make sure you find mentors like John to help you at at the appropriate stages.

As Josh suggested, when you first start your business you should focus on building systems and processes that allow you to accurately capture as much data as possible from the start. QuickBooks and other accounting software programs will do this for your finances, but you should also implement tools for tracking other key metrics (e.g. customer behavior, support inquiries, marketing analytics). You can and will become increasingly sophisticated in analyzing and interpreting that data over time, but you cannot analyze it if you do not have it.

Additionally, at all points in the development of your startup – including on Day 1 – you should focus intently on forecasting your cash flows as accurately as you possibly can. Running out of cash will either kill your company or force you into a very painful financing round. Know exactly when you run out of money, well before the time you hit a wall and go splat.

Finance Fridays: Getting Started – Allocating Equity and Founder’s Investment

Finance Friday’s gets off the ground with today’s post by introducing you to an imaginary startup, the entrepreneurs that we’ll being following throughout the series, and their first challenges: splitting up the founders’ equity and addressing the case where one of the founders provides the initial seed capital for the business.

We felt like we needed to put some groundwork in place using a case-study like approach, rather than just jumping into looking at balance sheets, income statements, and cash flow statements. Hopefully, by the time we are done, we’ll all have some new friends and a lot of knowledge. Let’s get started.

Jane and Dick worked together at Denver Health, the nation’s “most wired” hospital according to Hospitals & Health Networks Magazine. They have seen first-hand the impact technology can have in the medical field through exposure to a number of Denver Health IT initiatives. Through a series of conversations, Jane and Dick have come up with the idea to develop a social network tailored to the medical community. Through an online platform, doctors, nurses, and administrators would be able to assist each other with complicated diagnoses, collaborate on research studies, and find and fill job openings. After sharing the concept with a number of colleagues and receiving enthusiastic support for the idea, Jane and Dick built up the confidence to quit their day jobs and launch a business together.

Jane and Dick each brings a similar level of skill and capability to the business, making it easy for them to agree to a 50/50 equity split. While they could both go without salaries for a year, Dick had no extra money to invest in the business. However, Jane was in a position to invest some of her savings into the startup. How could they treat Jane’s cash investment in the business in a way that was fair to both of them?

Jane could have covered expenses from her personal account for now, keeping track of the receipts, with the plan of letting an accountant sort it out later. After all, they needed to focus on building their product, right?

Fortunately, Dick and Jane had both read Dharmesh Shah’s piece on avoiding co-founder conflict in Do More Faster and knew it was important to address co-founder issues – including how to handle co-founder investments – from the start. They also knew that it was important to set up proper accounting systems from the beginning and that paying for bills out of your personal bank account and having an accountant sort it out later for you seemed like a recipe for future pain.

Jane and Dick had several options, including structuring this as a debt transaction where Jane simply loaned the money to the company, or as convertible debt transaction where Jane’s investment would convert into equity in the next round. But they worried that future investors would frown on that or wouldn’t give Jane credit for the investment at a later date, since they might consider it as part of Jane’s contribution to her original ownership position of 50%.

That narrowed the possibilities down to an equity transaction, which would in turn require a conversation about valuation. Jane and Dick briefly considered a valuation based on the next external financing round, perhaps applying a discount. For example, if the first round of external investment values the company at $2 million post and, prior to that, Jane had invested $50,000, then with no discount, Jane’s investment would earn her 2.5% of the company ($50k/$2M = 2.5%). If they agreed on a 20% discount, then Jane would be entitled to 3.125% of the company ($2M * (1-20% discount) = $1.6M; $50k/$1.6M = 3.125%).

At this stage it wasn’t clear when (or even if) the first round of external financing might occur or what it might look like, which made agreeing on a discount just as difficult as agreeing on a valuation, while adding complexity. After a tense conversation about this, Jane and Dick decided to go out for a beer and try to resolve the equity allocation issue once and for all.

Jane indicated that the most she could invest in the company before they would have to seek other sources of capital was $50k. Dick hated to think that he would be diluted by more than 20% of his stake over $50k and proposed that Jane receive 10% incremental equity for her $50k. Jane felt comfortable with receiving 10% for $50k, but no less, so they agreed on a $450k pre money valuation of their startup.

There are a number of ways Jane and Dick could have executed the equity transaction. The simplest would be if they agreed in the founders documents that they would both commit full-time to the business, Jane would contribute an initial $50k, and they would split the equity 55/45 in favor of Jane.

Dick and Jane have now successfully navigated their first finance challenge: dividing up the founders’ equity, including an investment from one of the founders. A few key lessons from today’s post are:

- Invest the time upfront to get the founders’ documents right. This will save a lot of pain down the road. This includes agreeing on how you will handle personal investments in the business, but it also includes many other topics such as founders’ vesting schedules and voting rights.

- Every time you put money in the business it represents some form of debt or equity transaction. You can introduce complicated mechanisms for handling these transactions (e.g. warrants or discounts). However, there is a lot to be said for keeping things simple during the early stage of a startup. It helps control transaction costs in terms of both time and money.

- You could inject more cash into the business on an as-needed basis. However, this is distracting, even if you are raising the money from yourselves. Each cash injection effectively represents a new round of financing, which can get messy. Try to minimize the frequency of transactions by investing enough money each time to get you to the next key milestone for your business.

Next week, we will address how Jane and Dick put proper accounting systems in place. Oh, and you’ll notice that they don’t yet have a name for their company. They’ve told us they are open to suggestions.

Last week I expressed my frustration with the current lack of financial literacy that I see all around me. In the spirit of Fred Wilson’s awesome blog series MBA Mondays, I’ve decided to write a series of posts about this and asked for suggestions. I got a bunch, but one that stood out was from a group of incoming MBA students at the University of Chicago Booth. Their suggestion was to write a series of posts that follows the development of an imaginary startup as the company navigates various events, focusing on how each event will impact not only the P&L, but also the Balance Sheet and Cash Flow Statement.

I thought this was a great idea, so I engaged Jonathan, Simon, Kevin, and Kevin (you can meet them below) to help out. They are going to help me prepare the posts each week, which will include developing excel spreadsheets that we will upload to complement the posts. They suggested we call this “Finance Fridays” to bookend Fred’s MBA Monday’s – I checked with Fred to see if he was ok with this and his response was “Hell yes. The more the merrier.”

We would love to get your suggestions in the comments section for (1) the type of company that we should follow, and (2) the types of issues that the company might encounter (reminder: the goal is to illustrate common difficulties entrepreneurs face when it comes to understanding their financials). At this point we are planning to use a consumer Internet company as an example, but we are also considering using a SaaS-based software company.

As a special bonus for me, I get to work with four students on a project. I love working with and mentoring students, and am especially thrilled when they proactively reach out to me.

Our first substantive post will be up next Friday. In the mean time, please meet the Finance Fridays team:

Jonathan Wolter has been a lead consultant and software engineer at ThoughtWorks working for clients in Silicon Valley, Texas, Chicago, and India. Now he is slated to enter Booth at the University of Chicago in the fall. On the side, he started a company selling accounting training to landlords. Previously he was at FeedBurner, and has never met a side project he did not love.

Kevin O’Leary has spent the past year working as an independent financial consultant to start-ups in the healthcare, telecom and nonprofit industries on projects both domestically and internationally. Prior to that, he was an investment banking analyst in the Medical Devices group at Piper Jaffray. He will be entering Booth as an MBA Candidate this fall.

Simon Zhang spent three years as a financial and tax consultant at Deloitte Canada with a focus on businesses in mining, financial services and technology sectors. He is a Canadian Chartered Accountant. He also lectured an undergraduate tax course at Simon Fraser University and frequently facilitated professional education courses with Canadian Institute of Chartered Accountants. With a strong interest in entrepreneurship and technology, he subsequently joined a technology start up project at Orbis Investment Management Ltd, an asset management firm with over USD $25 billion under management. His focus was to incubate an internal start-up which is built on state-of-the-art technology, novel business model and innovative products. He will be entering Chicago Booth to complete this MBA with a focus on entrepreneurship and finance in the Fall 2011.

Kevin McCaffrey left his job as a strategy consultant in the Chicago office of McKinsey & Company to found Dot-to-Dot Children’s Books, a nonprofit social enterprise that works with children around the world to develop children’s books that are marketed to raise funding and awareness for the authors’ communities. Dot-to-Dot relies entirely on earned income and employs a unique cause-related marketing strategy designed to establish a successful position in the competitive children’s lit market. Kids from eight countries, including Cambodia, Eastern DR Congo, and Afghanistan, have participated in Dot-to-Dot projects. Kevin’s experience with Dot-to-Dot has him hooked on entrepreneurship, which will be his focus at Chicago Booth.