Does the Rule of 40 Work for Hardware?

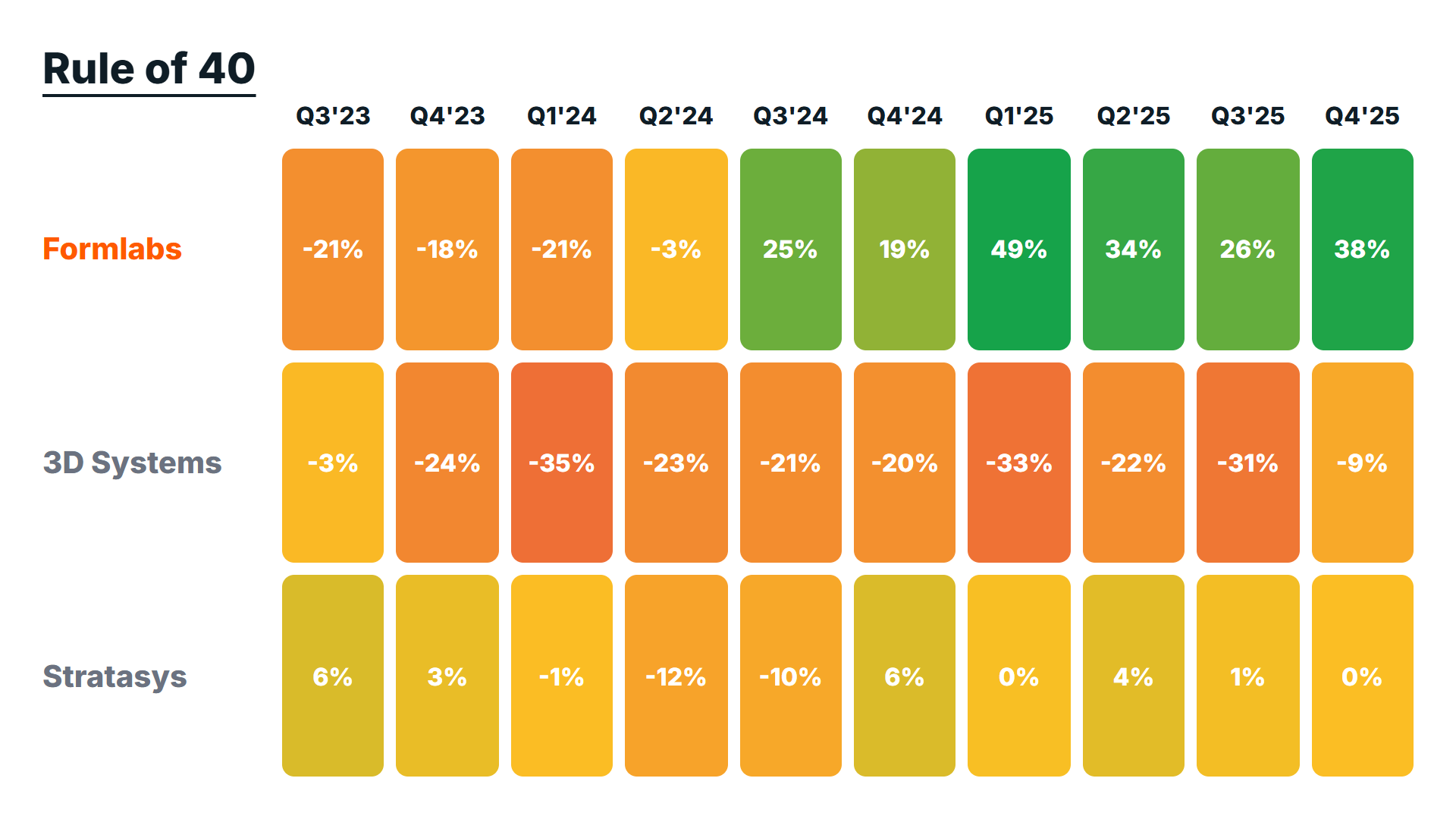

I've written about the Rule of 40 since 2015, and it's now gospel in SaaS. Does it mean anything for a company that makes physical things? Yes - but you have to read the curve, not the snapshot.

I've written about the Rule of 40 since 2015, and it's now gospel in SaaS. Does it mean anything for a company that makes physical things? Yes - but you have to read the curve, not the snapshot.

Eric von Hippel taught me that innovation comes from users, not manufacturers. My premise: all future end-user software innovation will come from the user, and the machines will build it.

On April 29 at 10am PT, Eric Ries and I are doing a free fireside chat for startup communities. We're going to talk about the lessons we've learned as founders, investors, and advisors - and the books we've each just put into the world.

I’m helping MIT (Fiona Murray and Alon Shklarek) share a short survey exploring how founders around the world navigate ethical challenges. Insights will shape practical tools for entrepreneurs, invest

I learned how to do deals from Len Fassler. Last week, I got an email from Dustin Kloempken, who sent me a few quotes he wrote down from the Berkshire

I’m not a sports fan, but wow, this is good.

On Tuesday, David Cohen (Techstars co-founder/chair) and I did an AMA for Techstars founders about the SVB crisis. The team at Techstars turned it into a podcast for our Give

GlueCon will occur for the thirteenth time, on May 24th-25th, in Broomfield, Colorado. My Foundry partners and I helped Kim and Eric Norlin create Gluecon in 2009 because we saw the need

For those of you older than 40, it sort of felt like 2000. If you are younger than 40, a massive tech bubble just burst. I expect you know that.

The 2nd Edition of my book Startup Boards: A Field Guide to Building and Leading an Effective Board of Directors launched today. My co-authors, Matt Blumberg, the CEO of Bolster,